What is smimodel?

The smimodel package provides functions to estimate

Sparse Multiple Index (SMI) Models for nonparametric

forecasting or prediction. To support time series forecasting, the

package functions are mainly build upon tidy temporal data in the

tsibble format. However, the SMI model formulation is very

general and does not exclusively depend on any temporal features. Hence,

the model can be used more widely—even with non-temporal cross-sectional

data. (In such case, a numeric index (instead of a date or

time related variable) can be used when constructing the

tsibble.)

The SMI Modelling algorithm (i.e. the estimation algorithm of SMI model) that we implement here, simultaneously performs automatic predictor selection (“sparse”) and predictor grouping, which is especially useful in obtaining a parsimonious model in high-dimensional contexts.

How to use smimodel?

Here we present a simple example to illustrate smimodel functionalities. We use randomly simulated data, which we treat as time series data for the purpose of this illustration.

(Note: Since the SMI model estimation algorithm works with very limited amount of prior information, and handles automatic predictor selection and predictor grouping, the computational time for model estimation increases as the number of predictors and the number of indices increase. Therefore, we use a small simulated data set here as the example to reduce computational cost.)

Data simulation

Suppose we are interested in forecasting a response variable , which is an additive function of two nonlinear components involving five predictor variables and plus a normally distributed white noise component. Here, the variables and correspond to the first, second, third and fifth lags of respectively.

## Load required packages

library(smimodel)

library(dplyr)

library(ROI)

library(tibble)

library(tidyr)

library(tsibble)

## Simulate data

# Length of the time series

n = 1405

# Set a seed for reproduciblity

set.seed(123)

# Generate data

sim_data <- tibble(x_000 = runif(n)) |>

mutate(

# Add x_lags

x = lag_matrix(x_000, 5)) |>

unpack(x, names_sep = "_") |>

mutate(

# Response variable

y = (0.9*x_000 + 0.6*x_001 + 0.45*x_003)^3 +

(0.35*x_002 + 0.7*x_005)^2 + rnorm(n, sd = 0.1),

# Add an index to the data set

inddd = seq(1, n)) |>

drop_na() |>

select(inddd, y, starts_with("x_")) |>

# Make the data set a `tsibble`

as_tsibble(index = inddd)Note that here we create an additional numeric variable

inddd to serve as the index of the data set,

when we convert the data set into an object of class

tsibble.

Next, we split the data into training and test sets so that the models can be estimated using the training data set, and the fitted models can be evaluated on the predictions obtained for the test set, which is not used for model estimation.

## Data Split

# Training set

sim_train <- sim_data[1:1200, ]

# Test set

sim_test <- sim_data[1201:1400, ]

# Here, we sequentially split the data as we assume time series data. SMI model estimation

We first train SMI models on the training set using three different initialisation options “ppr”, “additive” and “linear” for comparison purposes. Please refer to package documentation/working paper for more information regarding available initialisation options.

(Note: The choice of the initialisation largely depends on the data and application. Thus, users are encouraged to follow a trial-and-error procedure to determine the most suitable initial model for a given application.)

Here, we assume that we do not have any prior knowledge about the construction of the response variable . Hence, we input and its first five lags as our predictor variables into the estimation algorithm, as predictors which are entering indices.

## Index variables

index.vars <- colnames(sim_data)[3:8]SMI model with “ppr” initialisation:

## SMI model with "PPR" initialisation

smimodel_ppr <- model_smimodel(data = sim_train,

yvar = "y",

index.vars = index.vars,

initialise = "ppr")

# Fitted optimal SMI model

smimodel_ppr$fit[[1]]$best

#> SMI Model Fit:

#> Index coefficients:

#> 6 x 2 sparse Matrix of class "dgCMatrix"

#> index1 index2

#> x_000 0.4636151 .

#> x_001 0.3055133 .

#> x_002 . 0.345222

#> x_003 0.2308716 .

#> x_004 . .

#> x_005 . 0.654778

#>

#> Response variable:

#> [1] "y"

#>

#> Index variables:

#> [1] "x_000" "x_001" "x_002" "x_003" "x_004" "x_005"

#>

#> Spline variables (non-index):

#> NULL

#>

#> Linear variables:

#> NULL

#>

#> GAM Fit:

#> Family: gaussian

#> Link function: identity

#>

#> Formula:

#> y ~ s(index1, bs = "cr") + s(index2, bs = "cr")

#>

#> Estimated degrees of freedom:

#> 8.5 6.1 total = 15.6

#>

#> REML score: -1028.854

# Estimated index structure

smimodel_ppr$fit[[1]]$best$alpha

#> 6 x 2 sparse Matrix of class "dgCMatrix"

#> index1 index2

#> x_000 0.4636151 .

#> x_001 0.3055133 .

#> x_002 . 0.345222

#> x_003 0.2308716 .

#> x_004 . .

#> x_005 . 0.654778SMI model with “additive” initialisation:

## SMI model with "Additive" initialisation

smimodel_additive <- model_smimodel(data = sim_train,

yvar = "y",

index.vars = index.vars,

initialise = "additive")

# Fitted optimal SMI model

smimodel_additive$fit[[1]]$best

#> SMI Model Fit:

#> Index coefficients:

#> 6 x 2 sparse Matrix of class "dgCMatrix"

#> index1 index2

#> x_000 0.4634955 .

#> x_001 0.3054954 .

#> x_002 . 0.3451773

#> x_003 0.2310091 .

#> x_004 . .

#> x_005 . 0.6548227

#>

#> Response variable:

#> [1] "y"

#>

#> Index variables:

#> [1] "x_000" "x_001" "x_002" "x_003" "x_004" "x_005"

#>

#> Spline variables (non-index):

#> NULL

#>

#> Linear variables:

#> NULL

#>

#> GAM Fit:

#> Family: gaussian

#> Link function: identity

#>

#> Formula:

#> y ~ s(index1, bs = "cr") + s(index2, bs = "cr")

#>

#> Estimated degrees of freedom:

#> 8.50 6.09 total = 15.59

#>

#> REML score: -1028.856

# Estimated index structure

smimodel_additive$fit[[1]]$best$alpha

#> 6 x 2 sparse Matrix of class "dgCMatrix"

#> index1 index2

#> x_000 0.4634955 .

#> x_001 0.3054954 .

#> x_002 . 0.3451773

#> x_003 0.2310091 .

#> x_004 . .

#> x_005 . 0.6548227SMI model with “linear” initialisation:

## SMI model with "Linear" initialisation

smimodel_linear <- model_smimodel(data = sim_train,

yvar = "y",

index.vars = index.vars,

initialise = "linear")

# Fitted optimal SMI model

smimodel_linear$fit[[1]]$best

#> SMI Model Fit:

#> Index coefficients:

#> 6 x 1 sparse Matrix of class "dgCMatrix"

#> index1

#> x_000 0.40811741

#> x_001 0.26853838

#> x_002 0.04185720

#> x_003 0.20411136

#> x_004 .

#> x_005 0.07737565

#>

#> Response variable:

#> [1] "y"

#>

#> Index variables:

#> [1] "x_000" "x_001" "x_002" "x_003" "x_004" "x_005"

#>

#> Spline variables (non-index):

#> NULL

#>

#> Linear variables:

#> NULL

#>

#> GAM Fit:

#> Family: gaussian

#> Link function: identity

#>

#> Formula:

#> y ~ s(index1, bs = "cr")

#>

#> Estimated degrees of freedom:

#> 7.8 total = 8.8

#>

#> REML score: -445.1356

# Estimated index structure

smimodel_linear$fit[[1]]$best$alpha

#> 6 x 1 sparse Matrix of class "dgCMatrix"

#> index1

#> x_000 0.40811741

#> x_001 0.26853838

#> x_002 0.04185720

#> x_003 0.20411136

#> x_004 .

#> x_005 0.07737565In this case, the SMI models fitted with “ppr” and “additive” initialisation options have correctly identified the index structure of the response by estimating two linear combinations (i.e. indices), while dropping out the irrelevant predictor . While correctly identifying as an irrelevant predictor variable, the SMI model estimated with “linear” initialisation however, has not correctly identified the index structure of the model—has estimated only a single index instead of the two indices.

Thus, as mentioned earlier, the final estimated model can change depending on the initialisation option chosen. Hence, the users are encouraged to experiment with different available initialisation options when choosing the best fit for the data/application of interest. (In a real-world problem (where the true model is unknown), it will be useful to fit SMI models with different initialisation options, and see which option gives the best forecasting/prediction accuracy.)

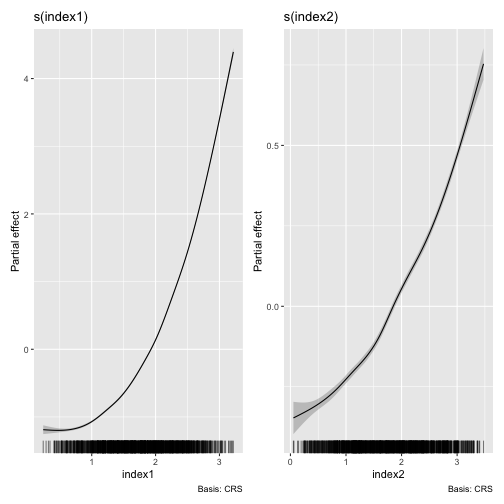

Visualisation of estimated smooths

Once you fit a SMI model, the partial effects of the estimated

smooths corresponding to the estimated indices can be plotted using the

autoplot method as below.

## Plot estimated smooths of the SMI model with "ppr" initialisation

autoplot(object = smimodel_ppr)

Residuals and fitted values

We can use the augment method to obtain the residuals

and the fitted values from an estimated SMI model.

## Obtain residuals and fitted values

augment(x = smimodel_ppr)

#> # A tibble: 1,200 × 3

#> Index .resid .fitted

#> <int> <dbl> <dbl>

#> 1 6 0.0566 0.757

#> 2 7 -0.0397 1.50

#> 3 8 -0.0552 3.78

#> 4 9 0.0499 1.78

#> 5 10 0.155 1.88

#> 6 11 -0.145 3.70

#> 7 12 0.200 2.16

#> 8 13 -0.00571 2.20

#> 9 14 -0.0585 2.78

#> 10 15 0.0690 0.588

#> # ℹ 1,190 more rowsForecasts on a test set

Based on an estimated SMI model, we obtain forecasts/predictions on a

test set as below, using the predict method.

## Obtain forecasts on the test set

preds = predict(object = smimodel_ppr, newdata = sim_test)

preds$.predict

#> 1 2 3 4 5 6 7 8 9

#> 3.45875259 1.52227838 0.52881104 2.24035158 1.12107147 1.37713685 3.45942510 1.29280288 1.30480760

#> 10 11 12 13 14 15 16 17 18

#> 0.76693416 0.94033375 1.69198167 1.19066341 1.31326856 1.62227903 2.32393332 0.83445703 1.04508990

#> 19 20 21 22 23 24 25 26 27

#> 1.18655331 4.77834376 0.61094061 1.14584964 0.79738240 1.40808298 2.33526200 0.17577515 0.55496943

#> 28 29 30 31 32 33 34 35 36

#> 0.36529819 0.86680931 0.58204728 0.07682039 0.12715469 0.59371085 2.34226095 0.88236602 0.31311292

#> 37 38 39 40 41 42 43 44 45

#> 0.47272680 0.98719807 1.08509641 1.63224918 1.08438592 0.94669238 0.69782251 0.29352743 1.42720367

#> 46 47 48 49 50 51 52 53 54

#> 1.80572138 1.56637665 1.60908623 0.46992486 0.52987039 1.75371557 0.35670514 0.52323854 2.84421134

#> 55 56 57 58 59 60 61 62 63

#> 1.52535348 1.21157098 1.57454092 0.35167609 0.81628181 1.16983691 0.14744439 0.76252668 3.59290968

#> 64 65 66 67 68 69 70 71 72

#> 0.41181444 2.45049844 1.07340894 0.95589469 2.55008954 0.60641501 3.72815494 1.90521972 2.62653129

#> 73 74 75 76 77 78 79 80 81

#> 2.97443784 1.17261901 1.32266114 0.58847194 1.53256266 2.14620254 1.74196253 2.66079827 0.79429653

#> 82 83 84 85 86 87 88 89 90

#> 2.20897818 1.95718405 1.04773411 1.37572254 2.27213107 1.86737728 0.84856583 2.17397767 1.42471476

#> 91 92 93 94 95 96 97 98 99

#> 0.92667153 2.26161088 2.21898501 3.09128273 2.79447124 0.60599090 1.10399804 1.38587451 1.84832772

#> 100 101 102 103 104 105 106 107 108

#> 2.95928627 1.75660705 0.83714657 0.44664008 1.24110982 0.44727137 0.43799614 0.43482032 1.11403760

#> 109 110 111 112 113 114 115 116 117

#> 0.90800010 0.98409355 0.77391461 0.92785753 1.44316813 0.53590956 0.70992483 0.71795358 1.41767391

#> 118 119 120 121 122 123 124 125 126

#> 1.35755259 2.13572836 2.08429360 2.88077416 0.93061594 2.19668318 0.26132355 1.22310358 1.28597904

#> 127 128 129 130 131 132 133 134 135

#> 0.54794253 1.30397046 1.46474006 1.18312452 0.66352232 1.22851353 2.41435557 2.60599716 2.59239098

#> 136 137 138 139 140 141 142 143 144

#> 0.97740761 1.39710803 1.03604458 0.73902008 1.11037088 2.98249685 1.16392033 1.56621624 2.29963520

#> 145 146 147 148 149 150 151 152 153

#> 1.45009245 1.01222387 0.19617259 0.24803096 0.17703054 0.24552278 0.11939235 0.06335250 0.78697563

#> 154 155 156 157 158 159 160 161 162

#> 0.77510661 0.44432578 2.11483463 0.36391308 1.84129095 1.72201999 0.56247570 0.86526871 0.15401982

#> 163 164 165 166 167 168 169 170 171

#> 0.86083789 0.36209679 0.16949950 0.38394360 0.08912956 0.44100934 0.88294634 1.29236413 2.58720558

#> 172 173 174 175 176 177 178 179 180

#> 1.48371732 3.04050479 1.20272911 1.04586676 2.14226125 0.44197929 2.79409719 0.52716239 1.55409562

#> 181 182 183 184 185 186 187 188 189

#> 1.42580960 0.36626185 2.72545139 0.29608435 0.87043136 2.92144635 1.94118373 1.64383166 1.23771152

#> 190 191 192 193 194 195 196 197 198

#> 0.96011483 2.37079432 2.37095016 1.44371807 0.58065932 0.37881098 0.50417286 0.34462475 0.18876236

#> 199 200

#> 0.20226401 0.26617350Once we obtain forecasts/predictions, we can evaluate the forecasting/predictive performance of the estimated SMI model by calculating forecast/prediction error measurements as desired.

Tuning for penalty parameters

The estimation of a SMI model involves solving an optimisation problem, where the sum of squared errors of the model plus two penalty terms (an L0 penalty and an L2 (ridge) penalty) is minimised subject to a set of constraints. Thus, two penalty parameters and corresponding to the L0 and L2 penalties respectively should be chosen when estimating a SMI model.

In the previous example, all the SMI models were fitted using the

default penalty parameter values provided in the function:

and

.

To fit a SMI model with simultaneous parameter tuning, we can use the

function greedy_smimodel(), which performs a greedy search

over a partially data-derived grid of possible penalty parameter

combinations

(,

),

and fits the SMI model using the best (lowest validation set MSE)

penalty parameter combination. In this case, we need to provide a

validation set, which is separate from the training data set.

Therefore, let’s split our original training set in the above example into two parts again to obtain a validation set.

# New training set

sim_train_new <- sim_data[1:1000, ]

# Validation set

sim_val_new <- sim_data[1001:1200, ]Next, we can estimate the SMI model with simultaneous penalty parameter tuning as follows. Here, we use the initialisation option “ppr” just to demonstrate the functionality.

## Estimating SMI model with penalty parameter tuning

smimodel_ppr_tune <- greedy_smimodel(data = sim_train_new,

val.data = sim_val_new,

yvar = "y",

index.vars = index.vars,

initialise = "ppr")

# Fitted optimal SMI model

smimodel_ppr_tune$fit[[1]]$best

#> SMI Model Fit:

#> Index coefficients:

#> 6 x 3 sparse Matrix of class "dgCMatrix"

#> index1 index2 index3

#> x_000 0.4632129 . .

#> x_001 0.3058459 . .

#> x_002 . . 1

#> x_003 0.2309412 . .

#> x_004 . . .

#> x_005 . 1 .

#>

#> Response variable:

#> [1] "y"

#>

#> Index variables:

#> [1] "x_000" "x_001" "x_002" "x_003" "x_004" "x_005"

#>

#> Spline variables (non-index):

#> NULL

#>

#> Linear variables:

#> NULL

#>

#> GAM Fit:

#> Family: gaussian

#> Link function: identity

#>

#> Formula:

#> y ~ s(index1, bs = "cr") + s(index2, bs = "cr") + s(index3, bs = "cr")

#>

#> Estimated degrees of freedom:

#> 8.43 4.30 2.99 total = 16.72

#>

#> REML score: -945.3404

## Selected penalty parameter combination

smimodel_ppr_tune$fit[[1]]$best_lambdas

#> [1] 0.01356766 0.01000000Here the selected penalty parameter combination is .